Monopoly Resources

Overview

In this topic, students will be introduced to monopoly. They’ll learn what a monopoly is, how it differs from perfect competition and what conditions give rise to it. They’ll also learn how monopolists decide on the profit-maximizing level of output and price. The social costs and benefits of monopoly will also be covered. In addition to monopoly, the topic will cover price discrimination.

Learning Objectives

- Define monopoly and identify real-world examples (11,16)

- Explain the key differences between monopoly and perfect competition (10,11)

- Discuss the causes of monopoly (6,8,11)

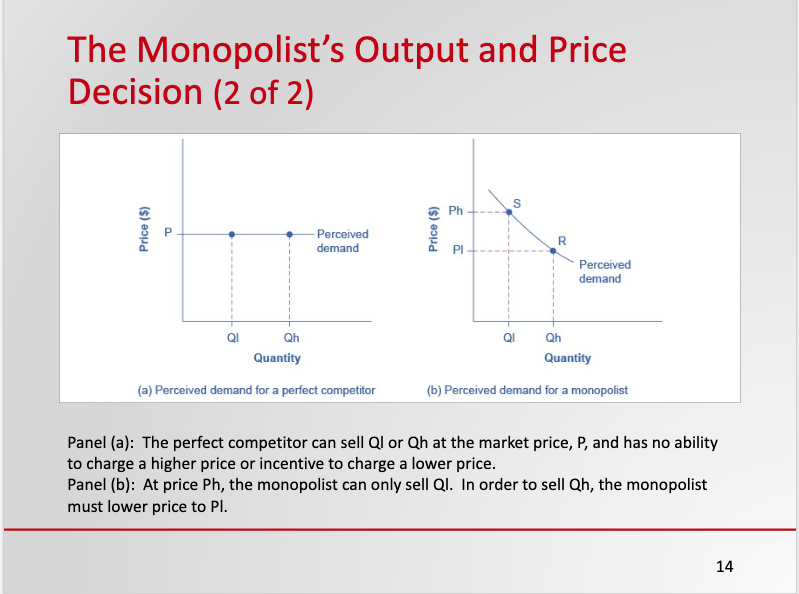

- Explain the demand curve faced by the monopolist and contrast it with the demand curve faced by the perfect competitor (5,10,11)

- Explain and demonstrate graphically how the monopolist maximizes profits (9,11)

- Discuss the problems caused by monopoly and identify possible solutions (4,6,11)

- Describe price discrimination and explain the market conditions necessary for it to exist (5,11,12)

- Describe how price discrimination affects business’ profits and consumer welfare (2,5,11)

NOTE: This Module meets Ohio TAG's 2, 4, 5, 6, 8, 9, 10, 11, 12 & 16 for an Intro to Microeconomics Course OSS004

Recommended Textbook Resources

Textbook Resources:

Principles of Microeconomics 2e

Full Citation: Greenlaw, S. and Shapiro et al. Principles of Microeconomics 2e. OpenStax CNX. June 4, 2018. OpenStax, Principles of Microeconomics 2e. License: Principles of Microeconomics 2e by OpenStax is licensed under Creative Commons Attribution License v4.0

- Chapter 9: Introduction to a Monopoly: This chapter covers learning objectives 1 through 6 and offers a good description of the conditions under which monopolies and how monopolists maximize profits. It also provides a good explanation of the allocation inefficiency created by monopoly.

Principles of Economics

Full Citation: University of Minnesota Libraries, Minneapolis, MN. Principles of Economics, Publishing Ed. 2016. University of Minnesota, CCA, 2016.License: Principles of Economics by University of Minnesota is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License, except where otherwise noted.

- Chapter 11.3: Extensions of Imperfect Competition: Advertising and Price Discrimination: Section 11.3 defines price discrimination and explains the conditions that must exist in order for a firm to practice price discrimination. The section also covers examples of price discrimination.

Video Resources

The following videos, which are produced by George Mason University also cover price discrimination.

- MR University “Introduction to Price Discrimination”: This video provides a good explanation of how price discrimination creates monopoly profits plus a description of the market conditions necessary for price discrimination to exist. Viewing time is 9:40 minutes.

- MR University “The Social Welfare of Price Discrimination”: This video looks at the social welfare implications of price discrimination and identifies conditions under which it is beneficial and conditions under which it is detrimental. Viewing time is 8:03 minutes.

Supplemental Content/Alternative Resources

Alternative Textbook Resource

Principles of Economics

Full Citation: University of Minnesota Libraries, Minneapolis, MN. Principles of Economics, Publishing Ed. 2016. University of Minnesota, CCA, 2016. License: Principles of Economics by University of Minnesota is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License, except where otherwise noted.

- Chapter 10: Monopoly: This chapter is similar in coverage and scope to the chapter on monopoly in the recommended text. Instructors may find useful examples in the chapter or may use it as a source for additional homework or discussion problems and questions.

Alternative Video Resources

The following two videos are produced by George Mason University. The selected videos are part of an extensive collection of videos that cover most topics in microeconomics.

- MR University “Maximizing Profit under Monopoly”: This video gives a good description of the types of barriers to entry that allow monopolists to maintain their market power. It also explains how monopolists maximize profits (it includes a short-cut for finding marginal revenue that doesn’t typically appear in principles texts). Viewing time is 11:10 minutes.

- MR University “The Costs and Benefits of Monopoly”: This video explains the deadweight loss due to monopoly but also considers the social benefits of granting temporary monopoly status to firms engaged in costly research and development. This video is embedded in the PowerPoint slides for this topic. Viewing time is 8:40 minutes.

Active Learning Exercise

Monopoly Power under Pharmaceutical Patents

In this exercise, students confront the issue of drug patents, which promote innovation but also create monopoly power. Students will read two New York Times articles about drug patents (references are provided) and answer questions regarding policy alternatives. The website includes instructor notes.

This exercise is included in Starting Point: Teaching and Learning Economics.

Questions and Problems

Monopoly

Questions and Problems

Questions

- Compare monopoly with perfect competition with regard to the following market characteristics:

- Number of sellers.

- Homogeneity of the good or service being sold

- Ease of entry into or exit from the industry

- Existence of market power

- Consider the following businesses or companies. Would you regard any of them as a monopoly? Why or why not? Could you use the monopoly model in analyzing the choices of any of them? Explain.

- Your local electric company

- The finest restaurant in town

- Your barber or hair stylist

- Your campus book store

- The U.S. Post Office

- During the life of its patent, from 1997 through 2011, the anti-cholesterol drug, Lipitor, made an estimated $100 billion for the drug company Pfizer. Critics claim that these earnings were a reflection of unwarranted monopoly profits. Others claim that the earnings were justified on the basis of gains in social welfare. Based on what you’ve read, can you make a case for one view or the other?

- Because monopolists control the entire supply they are often referred to as “price makers” meaning that they can decide what price to charge. Do profit-maximizing monopolists always charge the highest price? Why or why not?

- Imagine that the almond industry consists of many small growers, none of whom is big enough to influence the market price. Then, suddenly, all growers agree to pool their output and market as if they were a single seller. Compare and contrast the output and price of almonds before and after this sudden transformation.

- Why is the demand curve for a monopolist downward sloping while the demand curve for a perfectly competitive firm is horizontal?

- In order for price discrimination to be effective, three conditions must be met. Identify and briefly explain the importance of each of these conditions.

- Which of the following are examples of price discrimination? Explain.

- LL Bean offers a 20 percent discount on all sales, in store or online.

- Customers aged 65 and over receive a 10 percent discount at a dry cleaning store.

- A private university offers bigger tuition discounts to applicants with better scholastic records.

- “Big box” stores offer discounts for early shoppers on Black Friday

Answers:

- …

- A monopoly market consists of a single seller. A perfectly competitive market includes many sellers, none of whom is large enough to affect market price or quantity.

- A monopolist’s good or service must be unique or, at least, not have good substitutes. The perfect competitor’s good or service is identical to other sellers’ offerings.

- Entry into a monopolistic market is impossible (barriers to entry are high). Entry or exit to a perfectly competitive market is easy (barriers to entry are low).

- Defining market power as the ability to set price, a monopolist has complete market power. A perfect competitor is a price taker with no market power.

- …

- Your local electric utility is a natural (and regulated) monopoly. The technology underlying the production and distribution of electricity exhibits significant economies of scale which means that a single firm is likely to provide the most efficient service. The utility is regulated in order to prevent it from earning monopoly profits.

- “Finest” is a subjective quality that may allow the restaurant to charge higher prices but there is no significant barrier to entry so this is not an example of a monopoly.

- Barbers and stylists attempt to offer unique services and in most states, they must be licensed in order to provide services but there is no significant barrier to entry so they are not monopolists.

- In the past, the campus bookstore may have been the exclusive distributor of textbooks and other class materials, but with the rise of Amazon and other internet-based sellers, the monopoly power they may have enjoyed has likely diminished.

- The USPS has a monopoly on the delivery of first-class mail. The USPS provides a good example of the limits of monopoly power as technology has led to substitutes to first-class mail and reduced the value of the monopoly.

- The usual claim is that by establishing temporary property rights, patent protection offers firms the incentive to develop new drugs that will increase social welfare and that, without patent protection, firms will engage in less research and development than is socially optimal. Objections may arise over the length of the patent protection.

- Students should appreciate that even though monopolists can charge any price they wish, in order to maximize profits they must produce the Q at which MR = MC and charge the price associated with that Q. If they set a price higher than that, they will be selling a Q at which MR > MC, and thus foregoing additional profits.

- As perfect competitors, almond growers produced the quantity at which MR = MC where P = MR (each grower faced a horizontal demand curve at P). As a monopolist, the united almond growers still sell the quantity at which MR = MC but now they face the downward-sloping market demand curve so P > MR. Thus, the sudden change in structure leads to a higher price for almonds and because the market demand curve is downward sloping, a lower quantity.

- By definition, the monopolist IS the industry because it is the only seller. As a result, the monopolist faces the entire downward-sloping demand curve for its good or service. The monopolist has the ability to set price but can’t set price and quantity. A perfectly competitive firm is only one of many small firms in the industry selling a homogeneous good and must accept the going market price which is based on the intersection of the market demand and market supply curves. The perfect competitor can sell all she wants at the market price and has no ability to charge a higher price or incentive to sell at a lower price.

- First, the seller must face a downward-sloping demand curve. Perfect competitors are unable to engage in price discrimination: they can sell all they want at the market price but can’t sell any quantity at a higher price and have no incentive to sell at a lower price. Second, the seller must be able to segment the market into groups based on their willingness to pay and the willingness to pay must itself be different. The seller may segment the market by demographics or time of purchase or may just allow buyers to self-select. Third, the seller must be able to prevent buyers from engaging in arbitrage; that is prevent them from buying at the lower price and reselling to other buyers at the higher price.

- …

- This is not a case of price discrimination. The offer stands for all customers whether in store or online.

- This is a case of price discrimination because the discount is available only to a segment of the market. Sellers can require proof of age to maintain the price discrimination.

- This is a case of price discrimination. Students with superior scholastic records are likely to have more college choices and therefore, more elastic demand. Students with lesser scholastic qualifications are likely to have fewer college choices and less elastic demand.

- This is a case of price discrimination. Buyers willing to wait in line at odd hours are deemed to have a higher price elasticity of demand and are offered discounts. The discounts are only available for a short period of time.